Owning a home feels like you “made it” right up until the first year of bills starts landing like they’ve got a personal grudge, mortgage payment, property taxes, insurance, utilities, random stuff breaking at the worst possible time, and that delightful surprise called “closing costs” that somehow weren’t fully real in your brain until the lawyer emailed the total.

So let’s talk about the part nobody glamorizes: shaving dollars off the monthly chaos without turning your life into a full-time coupon hobby. You want real savings, not “download this sketchy extension and hope for the best” savings. Cool. Let’s do it.

Start With the “True Cost” of Homeownership (Because Your Mortgage Isn’t the Whole Bill)

Your mortgage payment (principal & interest) is loud and obvious, so it gets all the attention, while the other costs quietly pickpocket you every month, property taxes, hydro, natural gas, water, internet, home insurance, condo fees, and the steady drip of maintenance you can’t ignore forever.

That drip becomes a flood. Fast.

Grab a simple homeowner budget and split costs into: monthly fixed, monthly variable, and “I’ll cry later” annual/seasonal stuff (HVAC service, gutter cleaning, snow removal, pest control, appliance repairs). Call it a sinking fund if you want to sound tidy.

I call it the “stuff breaks” money.

Mortgage-Related Savings Levers (The Big Swing Stuff)

If you’re hunting for savings, mortgage strategy is where the grown-up dollars are, changing one percentage point or one fee can beat a year of coupon clipping, and it won’t require you to remember seventeen promo codes at checkout.

Math wins. Every time.

1) Renewal: Negotiate Like You Actually Mean It

Lenders love “loyal” customers because loyal customers accept whatever renewal letter shows up, sign it, and then complain about rates in group chats instead of shopping around, which is adorable but also expensive.

Don’t be adorable.

- Ask for a better rate (yes, literally ask), then compare against at least two other offers.

- Check features: prepayment privileges, portability, penalties (IRD can sting), and whether you’re locked into something awkward.

- Look for lender incentives: cashback promos, rate holds, and “we’ll cover some of your switching costs” deals.

2) Switching Lenders: Hunt for Real Credits, Not Marketing Confetti

Switch offers can be legit, discharge fee reimbursement, appraisal credits, legal fee promos, but they’re also packed with fine print, and that fine print is where “free” goes to die.

Read it anyway.

- Watch fees: appraisal, legal, discharge, title insurance, registration, and any weird admin charges.

- Do a breakeven check: monthly savings vs total switching costs, including penalties if you’re breaking early.

- Cashback mortgages can help cash flow, but sometimes the rate is higher, do the two-year math, not the first-month vibe.

3) Payment Tweaks That Don’t Hurt

Accelerated biweekly payments can shave interest over time, and rounding up payments (say, $1,942 to $2,000) is one of those “barely notice it” things that quietly helps if you actually stick with it for years.

Years. Not weeks.

And if you’ve got prepayment privileges, use them strategically. Tossing a lump sum at principal can be more satisfying than any coupon you’ll ever find for furnace repairs.

Also more effective.

Debt & Cash-Flow Optimization (Because 22% Interest Is a Thief)

Some homeowners are “mortgage-poor” not because the mortgage is insane, but because the rest of their financial life is dragging them under, credit cards, lines of credit, car payments, and a couple of “temporary” balances that never died.

That’s the leak.

If you’re paying high-interest debt every month, you can sometimes lower your total outflow by consolidating, refinance, HELOC, or second mortgage, depending on your credit, income, home equity, and your tolerance for risk.

Not sexy. Very useful.

- HELOC: flexible, often decent rates, but the payment discipline is on you (and people… aren’t always disciplined).

- Refinance: can lower blended costs, but watch break penalties and closing fees.

- Second mortgage: can be a tool for consolidation or urgent expenses, often faster than a full refi, sometimes pricier.

And yes, sometimes the bank says no, because your income is “unconventional,” you’re self-employed, your credit is bruised, or you need a fast close and the bank’s timeline is basically “see you in 8–12 business decades.” In those cases, getting a handle on private mortgage lender options in Toronto can be the difference between stabilizing your costs now and spiraling for another six months while bills stack up.

Bridge financing isn’t magic. It’s a lever.

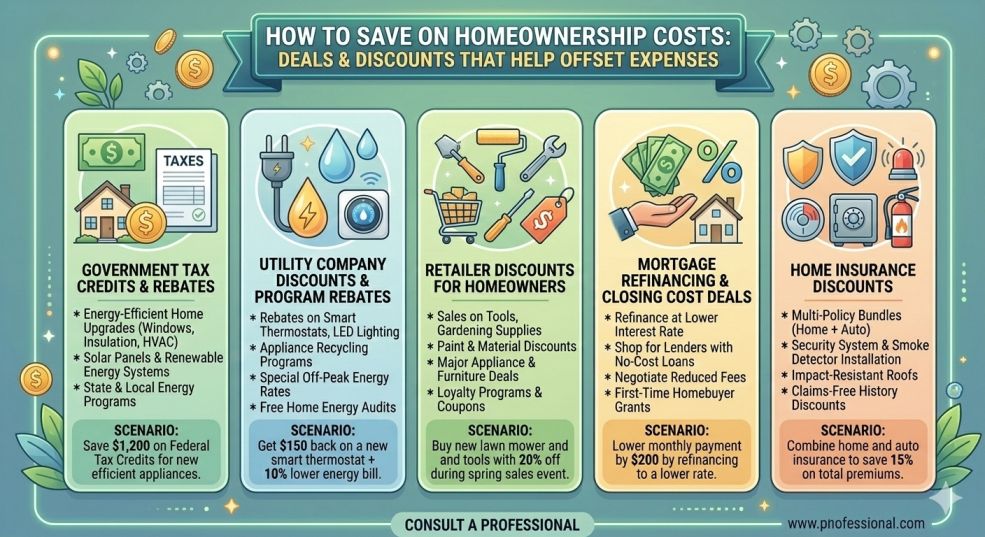

Deals & Discounts That Cut Monthly Carrying Costs (Without Wasting Your Life)

This is the fun part, the “pay less” categories where discounts actually show up, and you don’t have to refinance your soul to get them.

Still gotta be picky.

Home Insurance: Discounts Are Hiding in Plain Sight

Insurance discounts are boring, which is why people miss them, which is why they keep overpaying for years without realizing they were one checkbox away from saving real money.

Check the boxes.

- Bundle home + auto (usually the biggest discount).

- Higher deductible can reduce premiums, just don’t pick a deductible you can’t actually cover.

- Monitored alarm / security system discount (ask first, because not every system qualifies).

- Claims-free and new roof / updated electrical can help.

Quick move: call your insurer and ask, “What discounts am I not getting right now?” Then shut up and let them talk.

It works.

Internet & Utilities: Yes, You Can Negotiate

Internet providers have promos for new customers, and somehow they “can’t” give you anything until you ask to cancel, and then, wow, suddenly they have deals in a drawer.

Weird how that happens.

- Set a calendar reminder 10 days before promo expiry to renegotiate.

- Ask for current promos even if you’re an existing customer.

- Check competitor offers first so you’re not bluffing with nothing.

On utilities: small upgrades can cut bills without major renovation drama, LED bulbs, draft sealing, smart thermostat settings, and running big appliances off peak (if your pricing plan rewards it).

Cheap wins. Real wins.

Home Security, HVAC, Pest Control: Promo Pricing Is Common (But Read the Trap Terms)

Home services love introductory rates: “$99 tune-up,” “50% off first treatment,” “free install,” and then somewhere in the fine print there’s a contract, an auto-renew, or a “required subscription” that outlives your interest in the service.

Don’t get married to a coupon.

- Ask if it’s month-to-month before you book.

- Get the total annual cost, not just the first visit price.

- Check cancellation terms (fees are where the discount gets clawed back).

Home Improvement Stores: Stack Sales + Price Match + Loyalty Points

Home improvement retailers are basically built for stacking, sale price, clearance, “spend $X get $Y,” price match, and loyalty points, sometimes all in the same purchase if you’re not asleep at the wheel.

Don’t be asleep.

- Shop seasonal: insulation and draft stuff before winter, lawn gear end-of-summer, snow tools end-of-winter.

- Use price match when it’s allowed (and bring proof that’s not a blurry screenshot from 2019).

- Email sign-up discounts can be worth doing with a spare email address if you hate promo spam.

And if you’re buying appliances, always check: delivery, haul-away, warranty, and installation. The “deal” price is cute until the extras show up.

They always show up.

Energy Efficiency Rebates (Ontario/Canada): Don’t Pay Full Price for Comfort

Energy upgrades can be the rare home expense that pays you back, lower bills, better comfort, fewer “why is the bedroom freezing” fights, and rebates can soften the upfront hit if you follow the program rules.

The rules matter.

- Air sealing & insulation: usually strong ROI in older homes.

- Smart thermostat: not life-changing, but decent and easy.

- Heat pumps: bigger project, bigger potential savings, and rebates often exist depending on where you live and what you’re replacing.

- Windows/doors: comfort upgrade first, “save money” upgrade second (unless yours are truly awful).

One annoying detail: some rebates require an energy audit before and after. Miss that step and your rebate disappears.

Ask first. Buy second.

Property Tax & Municipal Costs: The Boring Bills You Can Sometimes Move

Property taxes feel non-negotiable, but assessments can be challenged in some cases, and municipalities have programs that can help certain homeowners (varies wildly, so you have to check your city, not a generic blog post from 2016).

Yes, it’s paperwork.

- Review your assessment and compare similar properties.

- Watch your water use, leaks are silent budget killers.

- Know your condo fees if you’re in a condo: special assessments are the “surprise party” nobody wants.

Maintenance Planning: Save Money by Being Slightly Paranoid

The cheapest repair is the one you never need because you caught the problem earlier, tiny plumbing drip, clogged gutters, furnace filter, caulking that’s falling apart around a window letting winter air punch you in the neck.

Small stuff. Big impact.

- Seasonal checklist: HVAC service, gutter cleaning, smoke/CO detector batteries, exterior checks after storms.

- Get 2–3 quotes for major work, and don’t hire the contractor who’s weirdly available tomorrow with a “cash-only” discount.

- Track lifespans: roof, water heater, appliances, none of them care about your budget timing.

And keep an emergency fund. Not a “maybe someday” fund, an actual one.

Because houses don’t wait.

Monetize the Property (If You’re Comfortable, Not Desperate)

If your monthly carrying costs are squeezing you, making the property earn money can be cleaner than constantly cutting and scraping, renting a room, a basement suite (follow rules and insurance requirements), or even renting parking/storage if you’re in the right area.

Just be realistic.

Being a landlord, even a casual one, comes with paperwork, boundaries, and the occasional “my friend is visiting for three months” conversation you didn’t ask for.

Plan for that.

Don’t Chase Discounts That Create Bigger Costs Later

Some “savings” are booby traps: stretching amortization just to get a smaller payment, taking on high-fee financing because you’re stressed, signing service contracts that auto-renew at premium rates, or buying cheap tools that snap the first time you actually need them.

Cheap can be expensive.

If you’re going to be a deal person (and you probably are, since you’re here), be the kind of deal person who reads the fine print, checks the total cost, and doesn’t let a promo distract from math.

That’s the whole game.