When most people think about Roth IRAs, they immediately focus on the tax-free withdrawals in retirement. And sure, that’s a significant advantage, but it barely scratches the surface of what makes this retirement account truly exceptional. Beyond the well, known benefit of tax-free growth, Roth IRAs offer a sophisticated collection of strategic advantages that can transform your entire financial planning approach. These hidden benefits span estate planning, flexibility in retirement timing, strategic tax management, and even healthcare cost mitigation.

Estate Planning Advantages That Preserve Family Wealth

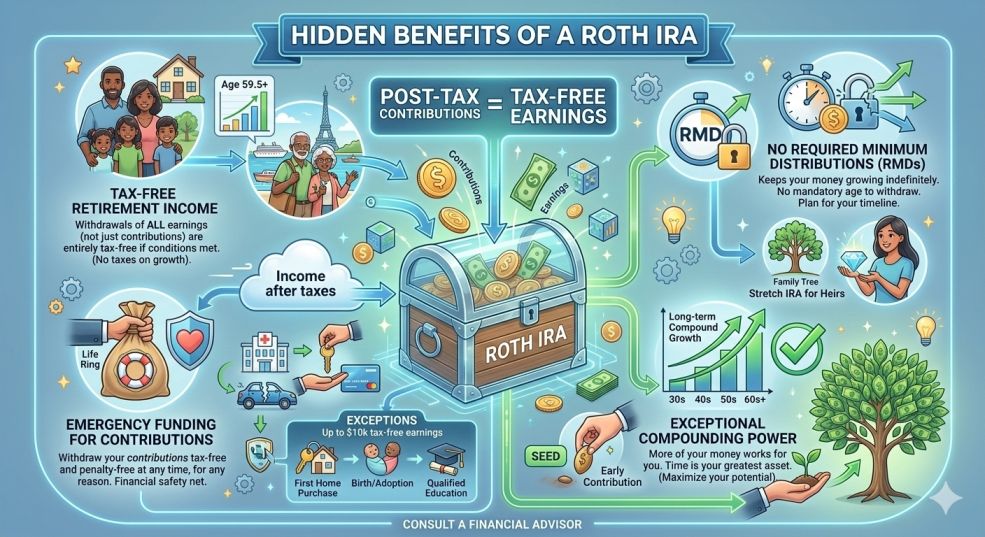

One of the most overlooked benefits of a Roth IRA is its exceptional value as an estate planning tool. Here’s what makes it different: unlike traditional IRAs, Roth accounts don’t require the original owner to take required minimum distributions during their lifetime. This means your savings can continue growing tax-free for as long as you wish, enabling you to preserve the account for your heirs rather than being forced to draw down the balance. When beneficiaries inherit a Roth IRA, they receive the distributions completely tax-free, a significant financial advantage compared to inheriting a traditional IRA where every distribution gets taxed as ordinary income.

Additionally, the absence of required minimum distributions means you can use other retirement accounts first, allowing the Roth IRA to serve as a legacy vehicle that continues growing without tax consequences. This strategic approach to wealth transfer makes Roth IRAs particularly valuable for individuals who have sufficient retirement income from other sources and want to maximize the inheritance they leave behind. It’s essentially a way to extend the benefits of your careful planning beyond your own lifetime, providing financial security for future generations.

Flexible Contribution Withdrawals Without Penalties or Taxes

Here’s a remarkably useful feature that few investors fully appreciate: the ability to withdraw your original Roth IRA contributions at any time, for any reason, without taxes or penalties. This flexibility creates an emergency financial cushion that traditional retirement accounts simply cannot match. While financial advisors generally recommend leaving retirement funds untouched, life sometimes presents unexpected challenges that require access to savings. With a Roth IRA, you can withdraw the amount you’ve contributed over the years without triggering the 10% early withdrawal penalty or owing any income taxes, regardless of your age.

This characteristic makes Roth IRAs particularly attractive for younger savers who may be hesitant to lock away money they might need for emergencies, down payments, or other major life expenses. The five, year rule applies to earnings withdrawals, but your contributions remain accessible throughout your life. This dual nature, serving as both a retirement account and a financial safety net, provides peace of mind that encourages more aggressive retirement savings among people who might otherwise be reluctant to commit funds long-term. It’s important to note that while this flexibility exists, the real power of a Roth IRA comes from allowing your investments to compound over decades, so withdrawals should remain a last resort rather than a regular practice.

Strategic Tax Diversification for Retirement Income Management

Many financial planners emphasize the importance of tax diversification in retirement, and Roth IRAs play a crucial role in this strategy that often goes unrecognized. Having sources of both taxable and tax-free retirement income? It gives you unprecedented control over your annual tax liability during retirement years. This flexibility allows you to strategically manage which accounts you draw from each year based on your specific tax situation, potentially saving tens of thousands of dollars over a retirement spanning several decades. For professionals who need to optimize their tax position while managing retirement distributions, a roth ira conversion can provide the foundation for this strategic flexibility.

In years when you need larger distributions for major expenses, you can withdraw from your Roth IRA to avoid pushing yourself into a higher tax bracket. Conversely, in lower-income years, you might draw more heavily from traditional retirement accounts to fill up lower tax brackets efficiently. This ability to control your taxable income becomes especially valuable when considering how it affects the taxation of Social Security benefits, Medicare premium calculations, and eligibility for various tax credits and deductions. Retirees with only traditional retirement accounts have no choice but to pay taxes on every dollar withdrawn, potentially triggering unwanted tax consequences.

Medicare Premium Protection Through Income Management

One of the most financially impactful yet commonly overlooked benefits of Roth IRAs relates to Medicare premiums and the Income-Related Monthly Adjustment Amount, commonly known as IRMAA. Medicare Part B and Part D premiums increase substantially for individuals whose modified adjusted gross income exceeds certain thresholds, with surcharges that can add thousands of dollars to annual healthcare costs. Because Roth IRA withdrawals don’t count as taxable income, they don’t contribute to the income calculations that determine these premium surcharges. This feature provides retirees with a powerful tool to manage their reported income and potentially avoid or minimize these expensive Medicare premium increases.

For individuals whose income hovers near IRMAA thresholds, the ability to draw tax-free income from a Roth IRA instead of taxable distributions from traditional accounts can mean the difference between standard Medicare premiums and significantly higher surcharges. The income thresholds for IRMAA can be triggered by relatively modest income levels, affecting many middle-class retirees who planned carefully but didn’t account for this particular expense. Over a twenty or thirty-year retirement, the savings from avoiding IRMAA surcharges through strategic Roth IRA withdrawals can easily exceed $50, 000 or more. This benefit becomes increasingly valuable as healthcare costs continue rising and Medicare premium structures evolve, making Roth IRAs an essential component of comprehensive retirement healthcare planning.

First-Time Home Purchase Exception for Young Investors

A particularly valuable benefit for younger Roth IRA owners is the first-time homebuyer exception, which allows for penalty-free withdrawals to purchase a home. After holding a Roth IRA for at least five years, you can withdraw up to $10, 000 of earnings, in addition to unlimited contributions, without penalty to help with a first home purchase. This exception applies to you, your spouse, your children, or even your grandchildren, making it a versatile tool for family financial planning. The definition of “first-time homebuyer” is surprisingly generous, too, you merely need to have not owned a home in the previous two years, meaning this benefit can potentially be used multiple times throughout your life.

This feature makes Roth IRAs particularly attractive for young professionals who want to save for retirement but also anticipate needing funds for a down payment within the next decade. The account serves dual purposes: growing retirement savings while simultaneously building a potential down payment fund. Even if you never use this exception, knowing it exists provides additional financial flexibility and reduces the psychological barrier that prevents many young people from prioritizing retirement savings. The ability to access these funds for homeownership without derailing your retirement plans represents a significant advantage over traditional retirement accounts that lack this specific exception.

Educational Expense Flexibility for Lifelong Learning

Another hidden gem within Roth IRA rules is the ability to make penalty-free withdrawals for qualified higher education expenses. While you’ll still owe taxes on any earnings withdrawn for this purpose, you avoid the 10% early withdrawal penalty that would otherwise apply. This exception covers expenses for you, your spouse, your children, or your grandchildren, including tuition, fees, books, supplies, and equipment required for enrollment. For families balancing retirement savings with education funding, this feature provides valuable flexibility and peace of mind.

Rather than contributing exclusively to 529 plans or other education-specific accounts, you can prioritize Roth IRA contributions knowing that the funds remain available for education if needed, but will support your retirement if not. This flexibility becomes especially valuable when children receive scholarships, choose less expensive educational paths, or decide not to pursue higher education, situations where dedicated education accounts may create complications. The Roth IRA’s education exception also applies to qualified expenses for part-time students and certain room and board costs, making it broader than many people realize. Additionally, grandparents can use this provision to help grandchildren with college costs while still maintaining control over their retirement assets, creating a multi-generational planning tool that serves both immediate family needs and long-term financial security goals.

Conclusion

The true power of a Roth IRA extends far beyond the commonly understood benefit of tax, free retirement withdrawals. From estate planning advantages that preserve wealth across generations to flexible access for emergencies, homeownership, and education, these accounts offer a remarkable combination of growth potential and strategic flexibility. The ability to manage Medicare premiums, diversify retirement tax obligations, and maintain control over your financial future makes Roth IRAs an essential component of comprehensive financial planning. Whether you’re just starting your career or approaching retirement, understanding and leveraging these hidden benefits can significantly enhance your financial security and provide options that simply don’t exist with other retirement vehicles.